We Have Brought Back Our 100k Tradeline Package For A Limited Time

We will add 100k in Au Tradelines to your Credit Report 6 lines in total with a combined credit age of 3 years. This Package is great for clients that are looking to get some funding with lines of credit and credit cards In the past we have sold this Package for $3495 but act now and you can get this package for only $2959. That's a savings of over $500.. Act Now there are Limited Spots Left Call or Visit us Today.. 323-776-6424 www.qualitytradelines.com/contact-us  A new card bumps up your total credit limit , so that you use less of it - provided your spending habits don’t change (sticking to a small monthly bill can ensure that). This will boost your score by improving your utilization

Plus, for each month you pay off your new card on time, you’ll get a positive mark on your credit report. Let’s say you only have one card that has a $10,000 limit and $5,000 balance. Your credit card use would be 50%- pretty high! But if you’re approved for a new card that also has a $10,000 limit, you can cut your use down to a healthier 25%. Is there anything to watch out for? Give your score time to grow

Did You Know That By Adding Some Of These High Limit High Age Tradelines You Can Boost Your Credit Score In 7-10 Day From The Report Date.. Call Or Visit 323-776-6424 www.qualitytradelines.com discover 15k limit 18yrs old reports 2nd jan. cost 850 2 spots discover 13900 limit 17yrs old reports 2nd jan cost 850 2 spots discover 15500 limit 18yrs old reports 3rd jan cost 850 2 spots citi bank 28k limit 13yrs old reports 3rd dec cost 970 1 spot citi bank 35k limit 10yrs old reports 3rd jan cost 1010 1 spot citi 20k limit 21yrs old reports 6th jan cost 1010 2 spots discover 15k limit 10yrs old reports 8th dec cost 760 2 spots citi 22k limit 29yrs old reports 8th of jan cost 1010 3 spots capital one 26k 16yrs old reports 9th jan cost 980 1 spot citi bank 10k limit 11yrs old reports 12th nov cost 750 2 spots barclays 16k limit 10yrs old reports 13th dec cost 750 3 spots citi bank 24k limit 23yrs old reports 16th dec cost 1010 3 spots capital one 27k limit 16yrs old reports 16th jan cost 1010 1 spot discover 10k limit 11yrs old reports 18th nov cost 750 1 spot citi bank 12k limit 24yrs old reports 18th jan cost 950 3 spots barclays 18k limit 12yrs old reports 19th jan cost 960 2 spot citi bank 22k limit 15yrs old reports 19th jan 19th jan cost 960 1 spot us bank 25k limit 14yrs old reports 26th jan cost 1010 2 spots us bank 25k limit 20yrs old reports 26th jan cost 1010 2 spots We Change Lives  1. Pay your bills on timeYour payment history accounts for approximately 35% of your credit score more than any other factor. If you have a history of paying bills late, you need to start paying them on time.If you've missed payments, get current and stay current. Each on-time payment updates positive information to your credit report. The longer your history of paying bills on time, the higher that portion of your credit score will be.

2. Review your credit report Errors happen, so review your credit report closely for:

If you find accounts that aren't yours and suspect you've been the victim of identity theft, you'll need to place a fraud alert on your credit report, close those accounts and file a police report and a complaint with the FTC. 3. Pay down your credit card balances The amount of debt you have is heavily scrutinized for your credit score. Your total reported debt owed is taken into account, as well as the number of accounts with outstanding balances and how much available credit has been used. The total reported debt is compared to the total credit available to determine your debt-to-credit ratio. Your credit score can suffer if those numbers are too close together. Your best plan for lowering your debt is to make a plan to pay it off. While it may seem like a wise move, don't consolidate debt onto one lower interest card. Credit inquiries and opening new credit can lower your credit score, at least in the short term. Closing old cards with high credit limits can also throw off your debt-to-credit ratio. If a new credit offer is too good to pass up, keep your total amount of credit available high by not closing any old credit cards. 4. Use credit You must use credit regularly for creditors to update your credit report with current, accurate information. While paying with cash or a debit card may make it easier to keep to a budget, a cash-only lifestyle does very little to improve your credit score. The easiest way to use credit is with a credit card, especially if you're trying to improve your score to qualify for an installment loan. If you have an old credit card, start using it responsibly again. A long credit history is a positive determining factor for your credit score, so making an inactive account active again may be advantageous. Although you need to make a point to use credit regularly, only charge as much as you can pay off. Keep your credit balances low so as not to damage your debt-to-credit ratio. 5. Monitor your credit report Keeping a watchful eye on your credit report will let you see if your hard work is paying off. Credit monitoring allows you to keep tabs on account activity. You'll also be immediately tipped off about any fraudulent activity. The credit bureaus and FICO® offer credit monitoring services, which typically cost about $15 a month to monitor all three of your credit reports and scores. If your Credit Score is not where you need it to be, give us a call or visit and we can look at your Credit Report for free and let you know what Tradelines will work the best for you Call 323-776-6424 or visit www.qualitytradelines.com  Have You Heard The Saying That You Have To Spend Money To Make Money?

Well The Same Is True About Credit.. You Need To Add Credit To Your Credit Report To Get More Credit.. Here Are Some Good TradeLines That Will Raise Your Credit Score With Limits And Great Age sept citi 10k limit 17yrs old reports 2oth cost 755 3 spots citi 12k limit 10yrs old reports 20th cost 755 1 spot capital one 10k limit 14yrs old reports 24th cost 755 2 spots citi 10k limit 16yrs old reports 24th cost 755 1 spot us bank 24500 limit 16yrs old reports 26th cost 950 2 spots citi 10k limit 16yr old reports 26th cost 755 1 spot oct captial one 28k 8yrs old reports on the 1st cost 855 1 spot discover 13k limit 16yrs old reports 2nd cost 755 2 spot discover 15k limit 18yrs old reports 2nd cost 855 1 spot discover 13900 17yrs old reports 2nd cost 755 1 spot discover 15500 18yrs old reports 3rd cost 855 1 spot Contact Us Today To Get More Credit On Your Credit Report www.qualitytradelines.com or call 323-776-6424 When you’re aiming for a better credit score, the last thing you want is to have your credit score take a hit. Unfortunately, little errors and mishaps can lower your score. One common reason for this is the “unauthorized credit inquiry”.

Essentially what happens, is that some unknown party does a credit pull and reviews your profile for an application that you may be unaware of. As strange and devious as it may seem, unauthorized credit inquiries happen more than most realize. Fortunately, you can prevent these mischievous little acts from affecting you. Who’s Fault is it Anyway? It’s one thing to accept a credit limit on an existing card or to ask for a loan. You know that a hard inquiry will follow. But what if you haven’t applied for any of the sort in months or years? How does a credit inquiry just appear on your profile? There are a number of parties that can cause these problems including:

The list goes on. However, the ones mentioned above tend to be the most common sources of problems. There are two issues that occur with these unknown credit pulls. First, the other party doesn’t openly inform you that they will pull your credit. Because of this, you may see no harm in agreeing to upgrade or accept an offer, especially if it seems to have some obvious benefits. Second, it’s easy to forget that you applied for these accounts in the first place. Many of these accounts won’t affect your finances in any major way, so you might hastily accept an offer, perhaps, while lined up at a store or talking over the phone. The Resulting Issues of Unauthorized Credit Inquiries There’s one major problem that comes with unauthorized credit pulls: a lower score. And as mentioned from the start, that’s the complete opposite of what you want if you’re looking to rebuild or maintain good credit. There is a trickle-down effect of course. The points that a series of unauthorized hard inquiries take off are usually low (around five or so). Nevertheless, they take you further away from the numbers that will get you approved for the best loans. And if you’re on the edge of loan approval, just a small deduction in points can mean that you no longer qualify. Serious indeed! Tips to Fight Unauthorized Credit Pulls and Avoid Them in the Future So how do you keep the hands of unwanted lenders and companies away from your credit profile? You have to stay ahead of them to beat them at their own game. To put it simply, everytime someone offers you an upgrade, store account or card, remind yourself that they could pull your credit without you knowing. That alone may help you decide whether you want to proceed or back off. It isn’t always this simple, however, and that means you might have to take things a bit further.

An unauthorized credit inquiry is frustrating to anyone, but even more so to the person who’s looking to improve their score. If it’s happened to you, don’t let it bring you too much stress. The number of points that they knock off is fairly small, and if you didn’t authorize the credit extension, you will likely have no issue proving that it’s fraudulent. More importantly, leave no stone unturned. Be diligent in your search for errors and ask as many questions as possible to get the info you need. In doing so, you will build a much stronger case for yourself. visit us at www.qualitytradelines.com if you have any credit questions  Generally, loan applicants with good credit qualify for larger loan amounts with lower interest rates. ... Fewer lenders will work with you if you have bad credit and those that do will charge a much higher interest rate on your auto loan. A higher interest rate means a higher car note to pay each month.

It Affects Where You Live and How Much You Pay Before you can buy a house, mortgage lenders want to know that you won’t default on your mortgage. If you don’t have good credit, the lender will consider it risky to give you a mortgage loan. If you're approved for a mortgage, your credit affects your interest rate which directly impacts your monthly mortgage payment. Bad credit could mean a higher mortgage payment. Worse than that, your mortgage application could be turned down because of your bad credit. Don't think that because you're not looking to buy a house right now that your credit isn't important. Landlords also use your credit to decide whether to rent to you. Landlords consider your lease as a loan. You’re being loaned a place to live and the landlord wants to know you’ll pay back this loan. If you don't have good credit, you can get denied for an apartment. It Affects What You Drive and Your Car Payment Unless you have the cash to purchase a car, you’ll have to get a loan. Your credit not only affects whether or not you qualify for a loan, but also the amount and interest rate of the loan. Generally, loan applicants with good credit qualify for larger loan amounts with lower interest rates. Bad credit limits your options. Fewer lenders will work with you if you have bad credit and those that do will charge a much higher interest rate on your auto loan. A higher interest rate means a higher car note to pay each month. It Can Affect Your Job Search Many employers conduct credit checks as a part of the hiring process. (Note that employers check credit reports not credit scores.) If you haven’t demonstrated financial responsibility, a prospective employer might be hesitant to hire you. For example, the employer might believe your level of debt is too high for the salary offered. It Affects Your Ability to Start a Business Many people have dreams of starting their own business. Most business startups require a sizable amount of cash that you might not have available. In that case, you’ll need to obtain a small business loan. Among other things, you need to have good credit to qualify for the business loan. It Affects Other Monthly Bills It might be somewhat shocking to learn that your credit is needed to establish utility service. Your electric company contends that you’re borrowing one month of electric service. So, before turning on your electricity, the company will check to see if you have good credit. This applies to most utility services including cable, telephone, water, and even cell phone. Since your credit is defined by how you’ve paid (or not paid) your bills in the past, many businesses — landlords, mortgage lenders, utility providers, and even employers — use your credit to predict your future financial responsibility. Anytime you need to borrow money, or even services, your credit is called into question. This is why maintaining good credit is so important. We can help you get your credit where it needs to be, give us a call or visit www.qualitytradelines.com 323-776-6424 One of the great ironies about wealth is that, for some people, more money is never quite enough. From those who struggle to pay rent, to millionaires who juggle speculative investments, anyone can feel a few dollars shy of true comfort. In reality, it often matters less how much you think you need, and more how you manage what you have.

When it comes to financial efforts — whether it’s saving for a major purchase, paying down debt, or simply living within your means — the trick is to create and stick to a plan. These four tips, if followed faithfully, will help you manage your money and provide more leeway in your approach to financial goals. 1. Set Goals and Create a BudgetGoals allow you to prioritize the truly important items on your financial outlook. Not all superfluous purchases occur at the mall; expensive entertainment subscriptions and restaurant meals also count, but many people simply accept these as normal expenses. Financial goals give you a reason to not spend money on unimportant things, and allow you to manage your finances more effectively. Write down and prioritize your goals, and organize them between short, medium, and long term. Short-term goals could occur within six months to a year, and can provide a framework for your budget. A budget marks significant progress in the management of personal finances. Once you know how much to set aside for expenses, you can utilize additional money management tips to make what remains go further. In order to create an effective budget, you must know what you spend on a daily, weekly, and monthly basis. “Your budget is perfectly useless if you don’t take time to properly record and track your expenses,” says Adrianna Abreu, a financial writer for Simple. “Make a habit of collecting receipts for everything you purchase. Don’t forget to account for items bought online and bills paid through automatic withdrawals.” Tracking your expenses will also reveal problem areas in your spending. To get started, make a record of every purchase over the course of a month. Ask for receipts and tally them at the end of each day, or keep notes on your phone. Chances are, you will identify at least a couple of areas where you consistently over-spend. 2. Use CashA further money management strategy utilizes some old-fashioned tech: cash money. Once you’ve figured out your necessary expenses, you can allocate discretionary income toward things like restaurant meals and entertainment. To avoid fudging your discretionary allowance — and throwing your budget out of whack — take the money out of your account once a month in cash. In addition to money management, you’ll find the use of cash can help manage the tedium of sticking to a budget. “To avoid budget burnout, withdraw cash to use toward discretionary purchases like coffee and movie tickets,” says Kendal Perez, savings expert with CouponSherpa.com. “Using cash to pay for fun means you’re still enjoying your money, but not sabotaging your goals.” Money reserved for discretionary spending allows for flexibility and fun. Unfortunately, it’s easy to lose sight of a budget when you simply put everything on a debit or credit card. If you find yourself consistently spending too much in certain categories, such as gas or groceries, you can use cash to help keep to your limits. If you worry about your ability to resist quick trips to the ATM, just leave your debit cards at home. 3. Automate EverythingSince it’s difficult to miss income that you never see, automated savings plans can become a boon for anyone who struggles to manage money. Most money troubles come from an inability to live within financial means; in other words, people spend more than they make. The only way to correct a negative savings rate is to dedicate income directly to savings. Again, return to your budget and identify some areas to make cuts. Once you find a number you’re comfortable with, set an automatic debit into a savings account for each pay period. You can start small, say $50 to $100 a month, and increase your savings gradually. If you get a raise, a good rule-of-thumb is to dedicate half the increased amount toward your savings. You’ll likely never notice the difference in your lifestyle, and will accumulate a nice nest egg as the months and years pass. If you struggle with forgetfulness, you can also automate many bills. An often overlooked money management skill, paying bills on time can save you both money and headaches. “Don’t just anticipate, automate,” says Chantay Bridges, financial coach and realtor with Truline Realty. “If you find yourself slipping, delayed, or hindered taking care of financial responsibilities, automatic bill pay will save you tons on late fees and higher interest costs.” 4. Prioritize Your DebtIf you have considerable debt, it can feel nearly impossible to manage your money effectively. Minimum payments and rising interest make it difficult to save money; without a savings, you must turn to credit for emergencies or unforeseen bills, thus worsening the debt situation. Throwing away money to interest does not represent effective money management. To avoid this, you’ll want to pay off your highest interest debt first, regardless of the actual balance compared to other debts. Once this occurs, you can move on to the next highest, and so on. To make the most of your efforts, contact your creditors and try to negotiate better terms. “You should always negotiate rates with credit card companies, or complete a balance transfer to find a credit card with an intro rate of zero percent,” says Sandy Young, founder of SY Financial Group. “Work towards paying off any high interest debts, then start saving and investing.” A few months of conscious effort will hopefully leave these money management tips permanently integrated into your behavior. As your debt decreases and your savings grows, you’ll see the positive proofs of your efforts. Though it can seem difficult at first, the establishment of good money habits will quickly transform saving into second nature. Have more questions? Contact us www.qualtiytradelines.com/contact-us  The first hour of work can either make or break your day. That’s right – what you do during this initial 60 minutes on the clock will often define all the presentations, strategy sessions and creative executions you do over the next eight (plus) hours. Let’s take a quick look at the ways successful people spend this hour, so you can emulate and win the day by winning the morning.

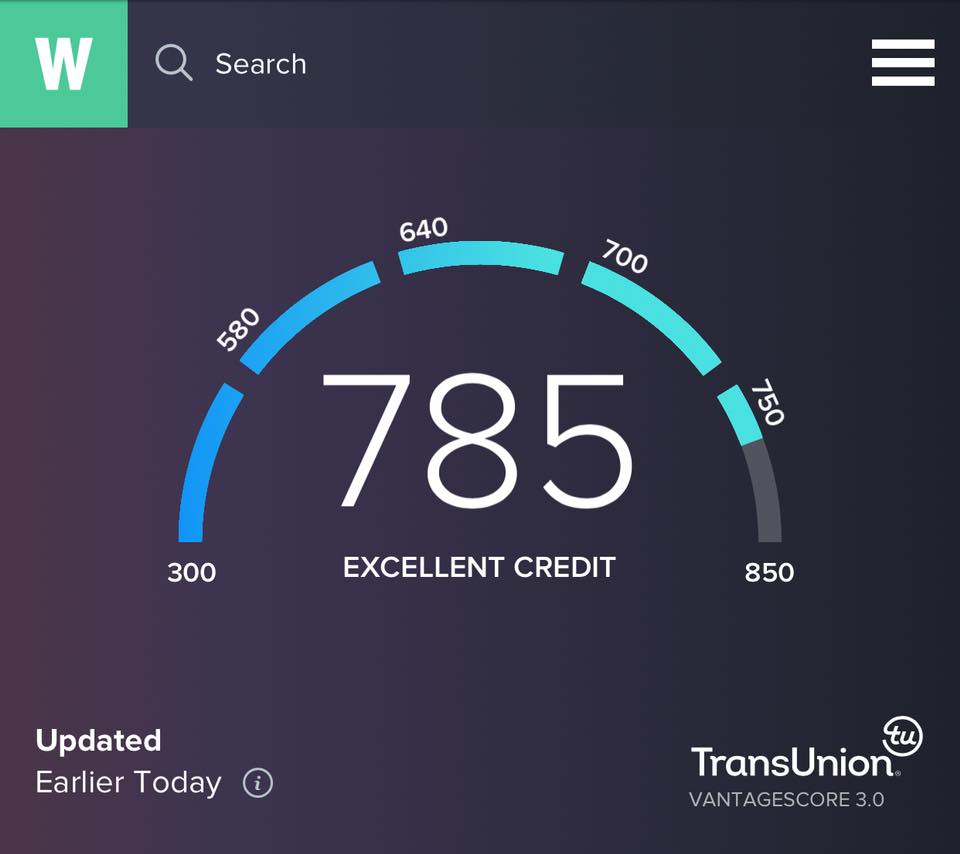

The Prework MorningWhile this article is about productivity, it doesn’t include tactics for being productive when you first get out of bed. If you’re looking for a guide to winning the morning before getting to work, check out this podcast from Tim Ferriss, author of “The 4-Hour Workweek.” Start Your Morning the Night BeforeThe best time to prepare for your morning is the day before. Spend some time thinking/meditating on your goals, both short and long term. From there, consider the tactics needed to make that happen. Kenneth Chenault, former American Express CEO, writes down a list of the top three things he wants to accomplish the next day before leaving his office. By doing this, he has a plan that he can focus on immediately when he gets to work the next morning. This is not the time to write down 100 things that would be nice to accomplish in the future. Instead, list the top three to five most important, game-changing goals for the day. This will help you prioritize and give you the ability to hit the ground running when you get to work the next day. Preparation is the most affective life hack for your mornings. Five-Minute VisualizationWhen your first get to the office, it’s easy to become overwhelmed by the multitude of tasks that are thrown your way. Before you jump into the hustle and bustle, spend a few minutes visualizing what you’re going to do with your day. Think about the things that would make this day a success and then visualize yourself completing these tasks and goals. Start by looking at your list from the day before. Have a successful day and get your credit report looking good in the upper 700 score Contact us today www.qualitytradelines.com or call 323-776-6424 |

QUALITY TRADE LINES

WE PROVIDE TRADE LINES & HELP YOU GET FUNDING WITH CREDIT CARDS AND LINES OF CREDIT Archives

June 2019

Categories |

RSS Feed

RSS Feed