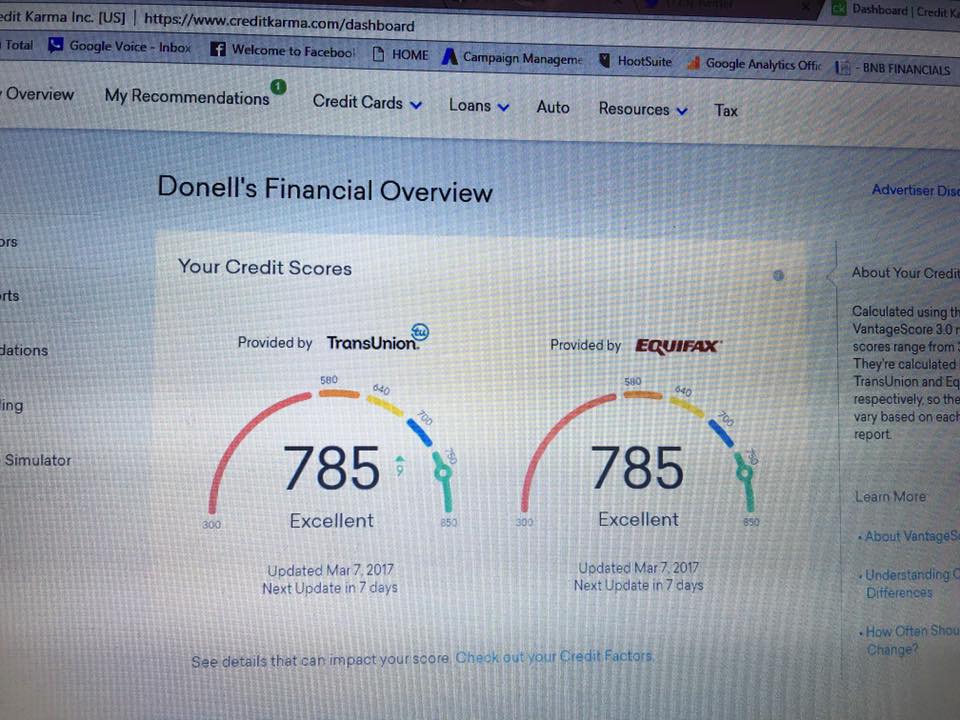

Did you know that by adding High Limit and High Age Tradelines to your Credit Report that you can get your Credit Score in the High 760-790 Range.... Here are some Tradelines that will help you get to where you want to be... call or visit today 323 776 6424 www.qualitytradelines.com/contact-us

citi bank 20k limit 6yrs old reports 3rd cost 680 citi bank 32500 limit 5yrs old reports 7th cost 680 discover 14k limit 13yrs old reports 7th cost 775 discover 12600 limit 12yrs old reports 7th cost 850 discover 14400 limit 23yrs old reports 9th costs 850 discover 17k limit 19yrs old reports 9th cost 850 discover 13k limit 22yrs old reports 9th cost 850 discover 13300 limit 20yrs old reports 14th cost 825 discover 12k limit 25yrs old reports 14th cost 850 discover 16500 limit 18yrs old reports on 14th cost 850 discover 14600 limit 30yrs old reports 14th cost 850 citi bank 10200 limit 39yrs old reports 16th cost 900 bank america 11500 limit 37yrs old reports 20th cost 900 citi bank 9400 limit 21yrs old reports 20th cost 750 discover 16500 limit 30yrs old reports 21st cost 900 citi bank 41k limit 8yrs old reports 21st cost 900 citi bank 10k limit 35yrs old reports 24th cost 900 us bank 21500 limit 20yrs old reports 26th cost 900 us bank 19k limit 10yrs old reports 26th cost 800 discover 15700 limit 31yrs old reports 28th cost 900

0 Comments

The Wells Fargo Cash Wise Visa® Card is terrific fit for anyone interested in a card with no annual fee and a big intro bonus that earns cash rewards and provides a 0% intro APR on balance transfers and purchases. If you need help with your fico score to be able to get this credit card visit us today www.qualitytradelines.com

Wells Fargo Cash Wise Visa® Card's intro bonus just increased from a nice $150 to a tremendous $200 cash back after you spend $1,000 in the first 3 months - a large bonus indeed. You'll also earn an ongoing unlimited 1.5% cash back on virtually all purchases. It's a convenient way to get cash rewards on everything you buy with your card, without having to sign up for rotating categories or jump through any additional hoops. As an added bonus, during the first 12 months you have your card you'll earn 1.8% back when using Android PayTM and Apple PayTM mobile wallets. Plus, your potential cash back is unlimited, so you can use your card as much as you want, knowing you won't run into any cash back limits. In addition to the cash rewards, the Wells Fargo Cash Wise Visa® Card features a 12-month 0% intro APR on both purchases and balance transfers. This can be very helpful in making any large (or small) purchases, as it gives you over a year of interest-free time help pay down your balance. It's almost like an interest-free loan for 12 months on things you buy with your card. Plus, if you're carrying a balance on other high-APR cards you can save some money but transferring your balance over to this card. There is an introductory balance transfer fee of 3% for 12 months, after that the fee is 5%. Although it's never fun to pay fees, it might be worth your while - to find out for sure either way use our free Balance Transfer Calculator. Wells Fargo Cash Wise Visa® Card includes an unusual and intriguing benefit - cellular (aka, mobile) telephone protection. This feature will reimburse you for damage or theft to your mobile phone, up to $600 per claim. There is a $25 deductible and a maximum of 2 claims in a 12-month period, but it's still a pretty awesome card perk. To qualify you just need to use your card to pay for your monthly cellular wireless telephone bill, which is pretty easy to set up with your mobile phone provider. All cardholders can easily redeem their cash rewards as a statement credit, for a paper check, for merchandise or gift cards, or for travel via their online portal. If you're a Wells Fargo customer, you can choose to direct deposit to your Wells Fargo checking or savings account, through a Wells Fargo ATM in $20 increments (note that you need a Wells Fargo Debit or ATM card to do this), via statement credit, or by requesting a paper check. You also have the option of applying your cash back as a credit to a qualifying Wells Fargo credit product like a mortgage or loan. Overall this is a great combination cash back and 0% intro APR card with a huge $200 intro bonus. Wells Fargo customers have more redemption options that non-Wells-Fargo-customers, although even if you're not a customer you can still get cash back via a statement credit or paper check. Or take a look at the non-bank-denominational Chase Freedom Unlimited card which also offers 1.5% unlimited cash back but a slightly lesser $150 intro bonus. Highlights

Rewards

Redeem Rewards

Fees and APR

Things you should know about VA loansThey are no down payments. One of the biggest advantages to a VA Loan is the fact you don’t need to put any money down. Yes you read that correctly! A VA mortgage is one of the few loan products where you can do 100 percent financing. This is great news for borrowers who do not have a ton of cash saved. They are flexible. There are few if any lending options available that can beat a VA mortgage. Long gone are the days when most people could walk up to a bank and get a loan for a home with no money down. That is, except for those that qualify for VA loans. With a VA loan you can still get a house for no money down – often even if you have previously been foreclosed on or filed for bankruptcy. This could be true even if it were a VA loan that was foreclosed on. This makes preparing to get a mortgage a lot easier for a borrower who has less than stellar credit. Need Credit Help Click Here There is a fee. All good things come with a cost. Although you can save a lot of money through securing a VA mortgage, you will have to pay a fee to get the loan. Known as the VA Funding Fee, this payment is used by the VA to keep the program running strong for the long haul. Typically charged at about 2 percent of your total loan amount, this fee can be rolled into your total loan, so you do not have to pay it out of pocket. If you have disabilities related to your service you may be able to get the fee waived. You avoid paying mortgage insurance. For most borrowers that take out a mortgage with less than 20 percent down, there is an additional cost to ownership – private mortgage insurance. This is an added cost that many lenders demand to protect their investment. When you use a VA mortgage loan, you are already guaranteed by the VA. Therefore you do not have to pay for the mortgage insurance. The VA is the guarantor, not the lender. It is important to understand that the VA is not the entity loaning you the money. You will get your loan from a standard lender like everyone else does. The difference is that the VA – with the backing of the Federal Government – guarantees up to a quarter of the amount you are borrowing. This makes lenders rest much easier – so easy that they are often still willing to loan to veterans with no money down. They are meant for your main home. The prospect of no-money-down real estate transactions is enough to get some people overly excited about purchasing a property. However, you should rein in any fantasies of building a real estate empire. VA loans are intended for service members to purchase their primary residence – not a vacation home or a restaurant. There are few exceptions, but not many. You are more likely to get a loan. This is a benefits program intended to help those that have served their country. Yes, you will have to meet a minimum set of requirements to get a loan. The lender will still want to know that you can repay what you borrow. However, you are more likely to get a VA loan – even with less than stellar credit – than you would be able to otherwise. As a bonus, the VA will often negotiate with lenders for you if you get behind on your payments. Theses are some of the more relevant facts regarding Veteran loans. So here are a couple of takeaways you should consider. If you are a seller and have received an offer from a buyer who would like to purchase your home using VA financing, don’t discount this as being a non-desirable way for a borrower to procure funding. Yes the downside is that the borrower does not typically offer much in the way of an escrow deposit. This is a risk a seller will need to take but the risk is usually worth it. The VA is a solid loan program that is no less desirable than conventional financing. If you are a buyer and are eligible for a VA loan, it is certainly something you should be considering! Let us know if you need some help with getting your credit ready www.qualitytradelines.com |

QUALITY TRADE LINES

WE PROVIDE TRADE LINES & HELP YOU GET FUNDING WITH CREDIT CARDS AND LINES OF CREDIT Archives

June 2019

Categories |

RSS Feed

RSS Feed