Did you know that by adding High Limit and High Age Tradelines to your Credit Report that you can get your Credit Score in the High 760-790 Range.... Here are some Tradelines that will help you get to where you want to be... call or visit today 323 776 6424 www.qualitytradelines.com/contact-us

citi bank 20k limit 6yrs old reports 3rd cost 680 citi bank 32500 limit 5yrs old reports 7th cost 680 discover 14k limit 13yrs old reports 7th cost 775 discover 12600 limit 12yrs old reports 7th cost 850 discover 14400 limit 23yrs old reports 9th costs 850 discover 17k limit 19yrs old reports 9th cost 850 discover 13k limit 22yrs old reports 9th cost 850 discover 13300 limit 20yrs old reports 14th cost 825 discover 12k limit 25yrs old reports 14th cost 850 discover 16500 limit 18yrs old reports on 14th cost 850 discover 14600 limit 30yrs old reports 14th cost 850 citi bank 10200 limit 39yrs old reports 16th cost 900 bank america 11500 limit 37yrs old reports 20th cost 900 citi bank 9400 limit 21yrs old reports 20th cost 750 discover 16500 limit 30yrs old reports 21st cost 900 citi bank 41k limit 8yrs old reports 21st cost 900 citi bank 10k limit 35yrs old reports 24th cost 900 us bank 21500 limit 20yrs old reports 26th cost 900 us bank 19k limit 10yrs old reports 26th cost 800 discover 15700 limit 31yrs old reports 28th cost 900

0 Comments

The Wells Fargo Cash Wise Visa® Card is terrific fit for anyone interested in a card with no annual fee and a big intro bonus that earns cash rewards and provides a 0% intro APR on balance transfers and purchases. If you need help with your fico score to be able to get this credit card visit us today www.qualitytradelines.com

Wells Fargo Cash Wise Visa® Card's intro bonus just increased from a nice $150 to a tremendous $200 cash back after you spend $1,000 in the first 3 months - a large bonus indeed. You'll also earn an ongoing unlimited 1.5% cash back on virtually all purchases. It's a convenient way to get cash rewards on everything you buy with your card, without having to sign up for rotating categories or jump through any additional hoops. As an added bonus, during the first 12 months you have your card you'll earn 1.8% back when using Android PayTM and Apple PayTM mobile wallets. Plus, your potential cash back is unlimited, so you can use your card as much as you want, knowing you won't run into any cash back limits. In addition to the cash rewards, the Wells Fargo Cash Wise Visa® Card features a 12-month 0% intro APR on both purchases and balance transfers. This can be very helpful in making any large (or small) purchases, as it gives you over a year of interest-free time help pay down your balance. It's almost like an interest-free loan for 12 months on things you buy with your card. Plus, if you're carrying a balance on other high-APR cards you can save some money but transferring your balance over to this card. There is an introductory balance transfer fee of 3% for 12 months, after that the fee is 5%. Although it's never fun to pay fees, it might be worth your while - to find out for sure either way use our free Balance Transfer Calculator. Wells Fargo Cash Wise Visa® Card includes an unusual and intriguing benefit - cellular (aka, mobile) telephone protection. This feature will reimburse you for damage or theft to your mobile phone, up to $600 per claim. There is a $25 deductible and a maximum of 2 claims in a 12-month period, but it's still a pretty awesome card perk. To qualify you just need to use your card to pay for your monthly cellular wireless telephone bill, which is pretty easy to set up with your mobile phone provider. All cardholders can easily redeem their cash rewards as a statement credit, for a paper check, for merchandise or gift cards, or for travel via their online portal. If you're a Wells Fargo customer, you can choose to direct deposit to your Wells Fargo checking or savings account, through a Wells Fargo ATM in $20 increments (note that you need a Wells Fargo Debit or ATM card to do this), via statement credit, or by requesting a paper check. You also have the option of applying your cash back as a credit to a qualifying Wells Fargo credit product like a mortgage or loan. Overall this is a great combination cash back and 0% intro APR card with a huge $200 intro bonus. Wells Fargo customers have more redemption options that non-Wells-Fargo-customers, although even if you're not a customer you can still get cash back via a statement credit or paper check. Or take a look at the non-bank-denominational Chase Freedom Unlimited card which also offers 1.5% unlimited cash back but a slightly lesser $150 intro bonus. Highlights

Rewards

Redeem Rewards

Fees and APR

Things you should know about VA loansThey are no down payments. One of the biggest advantages to a VA Loan is the fact you don’t need to put any money down. Yes you read that correctly! A VA mortgage is one of the few loan products where you can do 100 percent financing. This is great news for borrowers who do not have a ton of cash saved. They are flexible. There are few if any lending options available that can beat a VA mortgage. Long gone are the days when most people could walk up to a bank and get a loan for a home with no money down. That is, except for those that qualify for VA loans. With a VA loan you can still get a house for no money down – often even if you have previously been foreclosed on or filed for bankruptcy. This could be true even if it were a VA loan that was foreclosed on. This makes preparing to get a mortgage a lot easier for a borrower who has less than stellar credit. Need Credit Help Click Here There is a fee. All good things come with a cost. Although you can save a lot of money through securing a VA mortgage, you will have to pay a fee to get the loan. Known as the VA Funding Fee, this payment is used by the VA to keep the program running strong for the long haul. Typically charged at about 2 percent of your total loan amount, this fee can be rolled into your total loan, so you do not have to pay it out of pocket. If you have disabilities related to your service you may be able to get the fee waived. You avoid paying mortgage insurance. For most borrowers that take out a mortgage with less than 20 percent down, there is an additional cost to ownership – private mortgage insurance. This is an added cost that many lenders demand to protect their investment. When you use a VA mortgage loan, you are already guaranteed by the VA. Therefore you do not have to pay for the mortgage insurance. The VA is the guarantor, not the lender. It is important to understand that the VA is not the entity loaning you the money. You will get your loan from a standard lender like everyone else does. The difference is that the VA – with the backing of the Federal Government – guarantees up to a quarter of the amount you are borrowing. This makes lenders rest much easier – so easy that they are often still willing to loan to veterans with no money down. They are meant for your main home. The prospect of no-money-down real estate transactions is enough to get some people overly excited about purchasing a property. However, you should rein in any fantasies of building a real estate empire. VA loans are intended for service members to purchase their primary residence – not a vacation home or a restaurant. There are few exceptions, but not many. You are more likely to get a loan. This is a benefits program intended to help those that have served their country. Yes, you will have to meet a minimum set of requirements to get a loan. The lender will still want to know that you can repay what you borrow. However, you are more likely to get a VA loan – even with less than stellar credit – than you would be able to otherwise. As a bonus, the VA will often negotiate with lenders for you if you get behind on your payments. Theses are some of the more relevant facts regarding Veteran loans. So here are a couple of takeaways you should consider. If you are a seller and have received an offer from a buyer who would like to purchase your home using VA financing, don’t discount this as being a non-desirable way for a borrower to procure funding. Yes the downside is that the borrower does not typically offer much in the way of an escrow deposit. This is a risk a seller will need to take but the risk is usually worth it. The VA is a solid loan program that is no less desirable than conventional financing. If you are a buyer and are eligible for a VA loan, it is certainly something you should be considering! Let us know if you need some help with getting your credit ready www.qualitytradelines.com Chances are you’ve heard the term “credit score” before—every financial decision from applying for a credit card to getting a mortgage loan—is affected by your credit score. But what is a credit score exactly and why is it so important, especially for homeownership?

What is a credit score? Basically your credit score is a three-digit number generated using a mathematical algorithm. Where that number falls on a scale determines whether or not you have “good” credit. Your credit score is important because it lets lenders know if you’re “risky” to loan money to based on a number of factors. Most lenders rely on the FICO score, which ranges from 300 to 850—the closer to 850, the better! What factors affect your credit score? Your score is based on information on your credit report, which includes payment history, the amount of debt owed, how long you’ve had credit established, the types of credit you use, and new credit. How can you improve your credit score? There are a number of “good” actions you can take to improve your score, including:

Checking your credit score is easier now than it was in the past. Previously you could request a credit report from your bank for free once a year, but it didn’t always include your credit score. Now many banks and financial institutions offer the opportunity to check your credit score for free.Additionally, a lot of online services make it easy and convenient to check your score for free. How does your credit score affect homeownership? The biggest impact your score has on homeownership is your interest rate. Having a higher credit score typically means you’ll qualify for a lower interest rate because it tells lenders that you’ve been responsible about debt in the past. However, don’t be alarmed if your credit score isn’t great because there are a lot of other factors that lenders will look at including income, debt, and your front-end ratio. If you’re looking to purchase a home and worried about your credit situation, learn how you can start enhancing your credit here, and carry on the conversation on our social media platforms. Like and follow us on Facebook and leave us a tweet on Twitter. Improving your credit score is one of the best investments that you can make in your financial life.

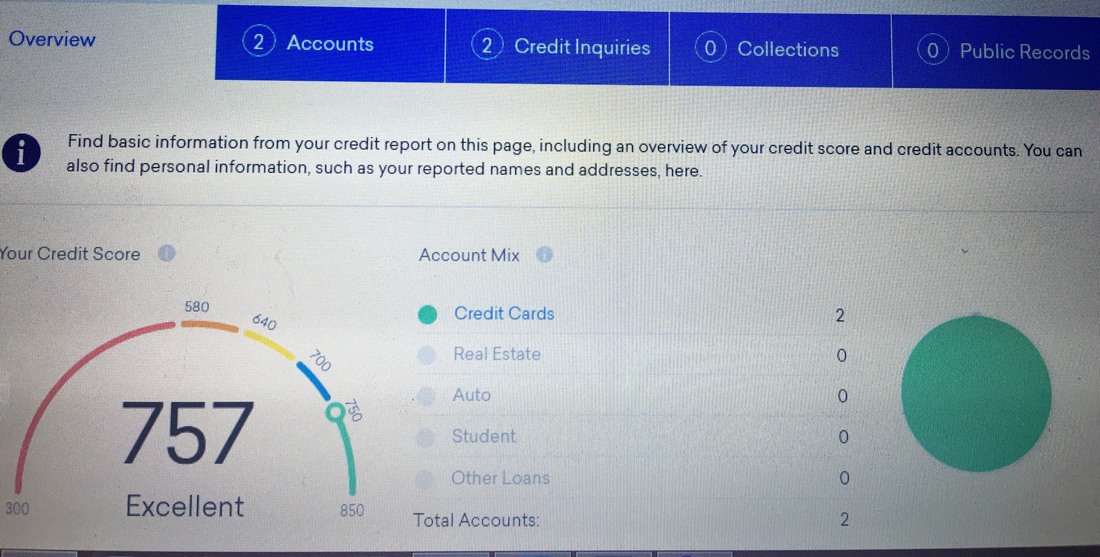

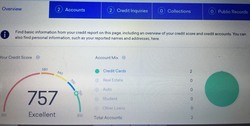

Your credit score may determine whether you qualify for a student loan, mortgage, auto loan or credit card. Your credit score also may be used when you apply for insurance, rent an apartment or purchase a cell phone. To maximize your chance for approval and to help obtain the lowest interest rate, here are five easy steps that you can take to boost your credit score: 1. Check your credit reports for accuracy It is essential that you obtain a copy of your credit report and check it carefully. The Federal Trade Commission found that 5% of consumers had one or more errors on their credit report. There are three major credit bureaus: Experian, Equifax and TransUnion. Each credit bureau collects information on your credit history and develops a credit score that lenders use to assess your riskiness as a borrower. Under federal law, you are entitled to view your credit report every 12 months from each credit bureau. Since each credit bureau may have different information about your credit history, your credit score may vary across the three lenders. For a free copy of your credit report, you can visit Annualcreditreport.com or Credit Karma. Credit Karma, for example, will provide your credit score and credit report from two credit bureaus: Equifax and TransUnion. If you find an error, you should report it to the credit bureau immediately so that it can be corrected. Your credit score will not improve over night, but the sooner you take action, the better. 2. Develop a financial track record If you already have a credit history, but want to improve your credit score, you need to demonstrate that you are financially responsible. To do so, you need to develop a financial track record in good standing. Credit card companies, for example, closely monitor both your payment history and account age (how long the account has been open in good standing). If you have a credit card, start by making small purchases and paying off the balance in full each month. The longer that you can keep open a credit card in good standing, the better (so that you can increase your account age). Consistent on-time payment history and a long account age demonstrate both financial discipline and responsibility. 3. Do not open or close multiple credit cards at once Opening multiple credit card accounts at once will result in several hard inquiries to your credit report, which can cause your credit score to drop (at least temporarily). Credit card companies also will view you as a risky borrower. Likewise, if you have multiple credit cards, do not close them all at once. Even better, if you have an older credit card and it does not have an annual fee, you should consider keeping it open to demonstrate a longer credit history. 4. Keep your credit card utilization low Lenders evaluate your credit card utilization, or the relationship between your credit limit and spending in a given month. If your credit utilization is too high, lenders consider you higher risk. Ideally, your credit utilization show be less than 30%. For example, if you have a $10,000 credit limit on your credit card, ideally you should spend less than $3,000 in a given month. If you can use cash in lieu of a credit card to reduce your credit utilization to 20% or even 10%, your credit score should be even higher. Here are some ways to manage your credit card utilization:

5. Pay your bills on time Paying your bills on time is a major contributor to your credit score. Whether it is your utility bill, rent or student loan payment, you should always pay your bills on time. Failing to pay your bill on time can hurt your credit. FICO scores are weighted more heavily by recent payments so you can "override" a past missed payment by developing a pattern of more recent on-time payments. Therefore, if you have a delinquent payment, pay off the balance. However, missing a payment altogether can stay on your credit report for seven years. To avoid a late or missing payment each month, enroll in automatic payment with your service provider. Some service providers, such as student loan lenders, provide a financial incentive when you enroll in auto pay. For example, you may be eligible for a 0.25% interest rate deduction with your student loan lender when you enroll in automatic payments. If you have a choice to enroll in auto pay with your bank or directly your service provider, choose your service provider to ensure that your payment arrives on time each month. if you have any questions about your credit score or would like some information on how to raise your credit score fast and easy call or visit 323 776 6424 www.qualtiytradelines.com As of July 1, the nation's three credit reporting agencies will remove and exclude certain negative information from credit reports. Tax liens and civil debts will no longer be reported on credit reports if the negative information does not include a customer's name, address and Social Security Number or date of birth.

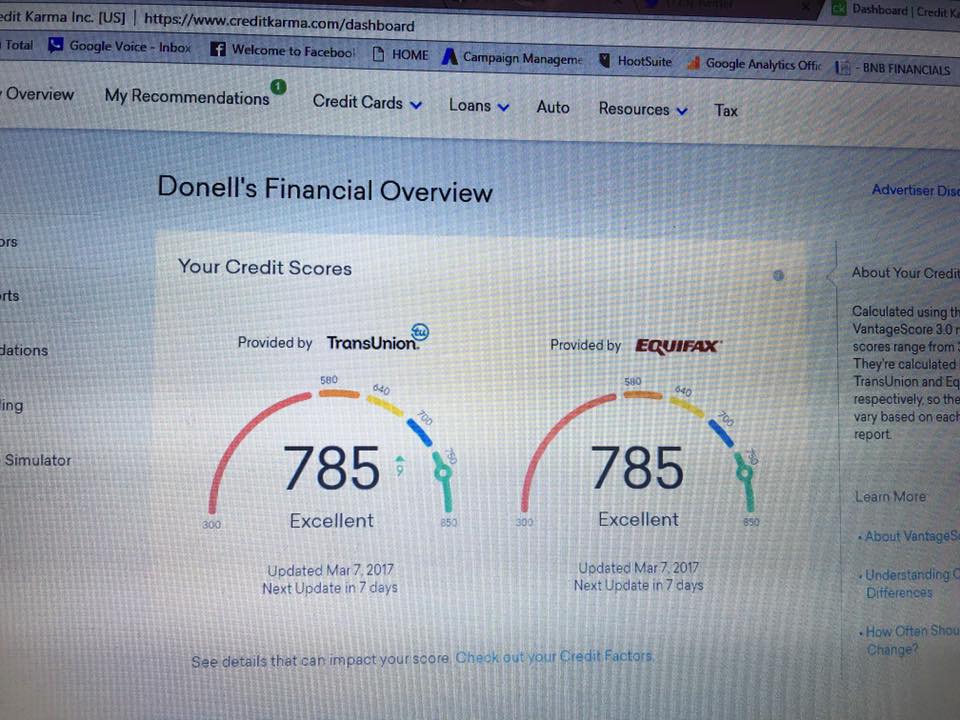

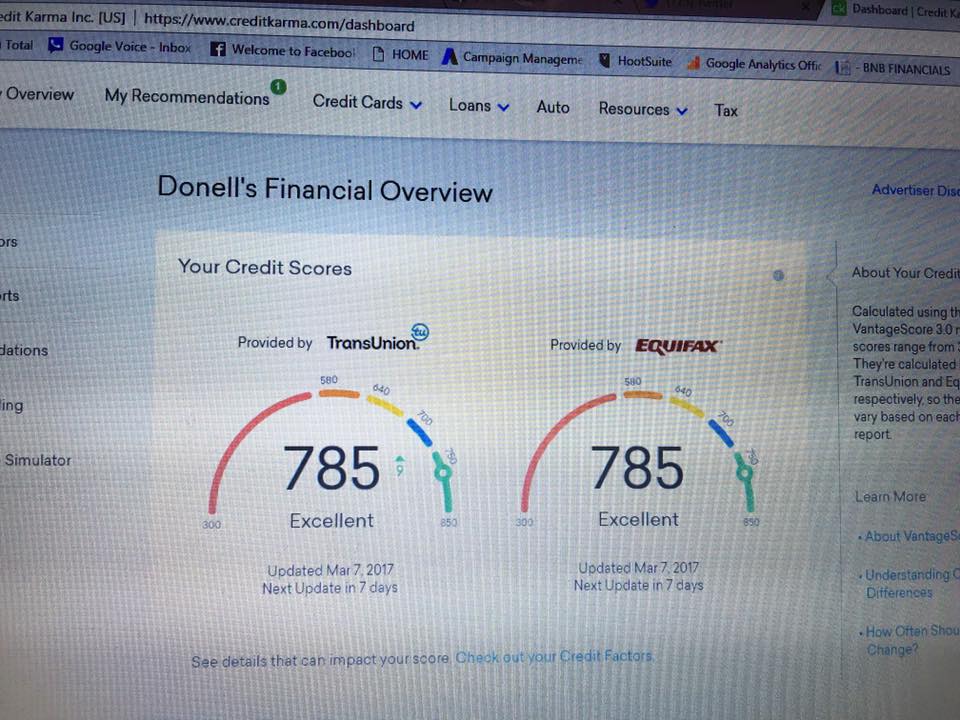

What Does This Mean For Me? Tax liens and civil debts can have a meaningful and negative impact on your credit score. According to FICO, although the impact of a tax lien diminishes over time, its presence on a credit report is "quite serious." Varous credit score simulators demonstrate that a tax lien could take as many as 100 points off your score, making it difficult to obtain credit or expensive if you do. If you have incomplete tax lien or civil debt records on your credit report, the removal should have a meaningful positive impact on your score. The change is supposed to happen on July 1, and you should see an immediate boost. Track your VantageScore for free at sites like CreditKarma. There are also a number of places where you can find your free FICO score, including from many credit card companies that offer the service to everyone (not just their customers). Why Is This Happening? One of the biggest complaint categories to the CFPB remains inaccurate information on credit reports. Under significant pressure, the credit reporting agencies are putting the burden of proof on the people and companies submitting negative information. These changes are not meant to reduce the negative impact of failing to make tax payments. Instead, the changes are meant to ensure that only accurate negative information is reported to the bureaus. Are There Any Downsides? For consumers in the short term, this will either be beneficial (to those people who have negative information removed) or neutral. However, there are some risks longer term. Having a tax lien on a credit report is highly predictive, and is a helpful indicator of credit risk. The reason people lose so many points from a tax lien is that the data shows how risky that behavior is. The downside is for lenders: now some risky people, with legitimate tax issues, will look less risky on credit reports. Over time, that could increase the default levels of better quality credit scores - driving up the cost of credit to everyone else in those better FICO buckets. Credit reports exist to ensure that the lowest risk people get the best terms and conditions. If higher risk people end up with lower risk scores, credit can become more expensive for everyone over time. Bottom Line There is a reason people complain about credit reporting agencies: there is too much sloppiness (at best) and fraud (at worst) in credit files. This recent move puts the burden of proof on people or entities filing negative information on credit reports. That is good news for consumers, and that is a good move long term. There is a short-term risk: people who legitimately avoided paying taxes benefit from the removal of negative information due to clerical errors. But that is still the right decision. If you cannot keep track of who owes you money, you shouldn't be able to file negative information on a credit report. contact us if you need to enhance your credit score by adding some tradelines 323 776 6424 www.qualitytradelines.com

Tradeline DefinitionA tradeline is an item on a credit report that refers to a past or present credit relationships. Tradelines include vehicle loans, credit cards, mortgages, leases, and other loans. A credit report lists separate tradelines for each account or credit card number, whether open or closed.

A seasoned tradeline is current with a history of timely payments. Some definitions state a seasoned tradeline is more than two years old. Credit Score DefinitionThe three major credit reporting agencies — Equifax, Experian and TransUnion — each report consumer credit scores. Equifax and TransUnion base their credit scores on a FICO formula. FICO is developed by Fair, Isaac & Co. Experian relies on a formula it developed and calls the PLUS Score. The three credit reporting agencies also use VantageScore, a competing score technology to FICO and PLUS Score. FICO, PLUS Score, and VantageScore are calculated using mathematical methods that incorporate credit history, amount of credit used and available, number of late and on-time payments, whether any payments due are in default, and other variables. The credit report lists specific accounts and financial history that go into the credit score. Proponents of FICO, PLUS Score, and VantageScore claim their scores are superior to the competition at predicting future consumer behavior. High number are supposed to indicate a high level of credit worthiness, whereas low scores represent a higher risk of default. FICO, PLUS Score, and VantageScore superiority claims are unsubstantiated because all three formulas are trade secrets and are impossible for third parties to test. Creditors and Credit ScoreCreditors use a person’s credit report when deciding whether to grant an applicant a line of credit or underwrite a loan. The easiest way to answer the yes or no question is to pick a number in a credit score as the threshold. Above a certain number puts the applicant in the maybe pile, and below a certain number merits a definite no. Piggybacking DefinitionAdding an authorized user to a strong account is known as piggybacking. Before 2007, authorized users got the benefit (or harm) from that account’s history. If a particular account’s history contained on-time payments and low account balances and a long history, the authorized user got the benefit of that strong history. Conversely, if an account was rife with late payments and high balances, the authorized user’s credit score was damaged. In 2007, Fair Isaac Company, the creator of the FICO score, reversed the long-standing policy of counting piggybacked accounts on an authorized user’s credit score. In 2008 Fair Isaac reversed the 2007 policy, and then in 2009 it announced another refinement when it rolled out FICO 08, the latest edition of its scoring algorithm. Buying or Renting a Seasoned TradelineA half-dozen companies and local entrepreneurs using Craigslist offer cash-rich but credit-score-poor consumers the opportunity to rent time as a authorized user on a seasoned tradeline. The cost varies, but $500 per tradeline is a common amount. The renter has no access to the seasoned tradeline account, and is not given the expiration date or three-digit security code on the account. The results, according to a 2010 Federal Reserve Board study of piggybacking are most effective for consumers who have a short credit history. Piggybacking can boost a consumer's marginal credit score into prime territory Is Piggybacking Legal or a Scam?From the consumer's perspective, piggybacking can result in the consumer qualifying for lower interest rates, which will save the consumer many thousands of dollars over the life of a mortgage or vehicle loan. Piggybacking is allowed and even expected by credit card companies between spouses and between parents and their children. If renting a seasoned tradeline keeps more money in a consumer's pocket by reducing interest costs, how is that a harm to the consumer? A consumer's lawyer will find there is no law prohibiting piggybacking between strangers. Credit card companies, in general, do not have policies prohibiting the practice. A FICO mathematician will almost certainly have a different perspective on the legitimacy question. Credit scores are meant to predict a consumer's credit worthiness, although credit scores are now sold to employers and insurance companies as tools to predict other behaviors as well. By gaming the system, the consumer boosts his or her credit score unfairly, which reduces the confidence level of the scores' predictive ability. Potential creditors want a cheap, easy, and reliable means of assessing the risk of potential borrowers. Creditors may argue that by gaming the system to allow less-creditworthy consumers access to prime loans, their eventual defaults raise the costs of loans for everyone. Creditors may be more reluctant to offer loans, or use more expensive means of determining creditworthiness. Regulators, such as the FTC, are tasked with protecting consumers. It is difficult to see how FTC regulation in this area would benefit consumers, unless the seasoned-tradeline brokers are not fulfilling their promises to rent the seasoned tradelines to customers. We keep our promises and add you to seasoned tradelines that report when they are supposed to and help you with your credit score. you can call us and we will look over your credit report and let you know what type and how many tradelines you will need to get the best for your credit report. call or visit us today to get on the better credit road office 323 776 6424 www.qualitytradelines.com  Get The Highest Credit Scores Possible

Keep your credit card balances below 5% of the credit limit to achieve the highest credit scores possible. What this means is if you're going to apply for credit, pay your bill down before the statement end date. Doing this will give you a low debt to credit ratio, which is a major factor in credit scoring.. Have a mixture of different kinds of Credit such as Revolving, Installment, Car and Home Loans will round out your credit and show Creditors That you are Credit Worthy Add some Positive Credit that has an older age and higher limits then you have now Call or visit us today and we can look over you credit report and tell you what you need to do to raise your scores and get the things that you want 323 776 6424 WWW.Qualitytradelines.com  Having a credit score in the high 700s and above will help you save money over time and allow you to get the credit you want when you need it. A few of the benefits of strong credit scores include:

Lower interest ratesThe interest rate you get is often directly tied to your credit score. If you have good credit scores, you’ll almost always qualify for the best interest rates on mortgage and auto loans. The interest rate you receive on a loan can make a substantial difference in your monthly payments and the total amount you will end up paying for your home or car. For example, just one or two percentage points less on your mortgage interest rate can save you tens of thousands of dollars over the course of the loan. Renting an apartmentLandlords often use credit scores to screen tenants and determine their financial trustworthiness. Credit scores can provide insight into how likely it is that you will pay your rent on time each month. A good credit score can increase your chances of getting into a house or apartment and prevent you from having to pay a higher security deposit. Insurance discounts Some car insurance companies factor in credit scores when determining monthly premiums. Although you can’t be turned down altogether for insurance based on credit scores, good credit scores can help you qualify for lower insurance premiums. Security deposits on utilitiesIf you are a new customer, utility companies may look at your credit report to get a sense of how likely you are to pay your utility bills on time. Having a good payment history and good credit scores will reduce the chances of needing to pay a security deposit when you establish utility service. Qualify for credit card rewardsExcellent credit will help you qualify for credit cards with low interest rates and other rewards including cash back offers, travel points and other types of incentives. Do you have questions about credit? Call or visit us today 323 776 6424 www.qualitytradelines.com  Why should you do business with us !! We Answer The Phone !! When You Call !! All The Time !! We have been providing Trade Line services for over 15 Years and we have seen how things have changed and will continue to change and we have been adapting ever since We can show you client scores and credit reports with our Trade Lines on the credit files. the same ones that you will be buying for your credit report We have some great Client Testimonials about our fast service and that the lines post when we say they post We can take your payment a few different ways. You can pay by credit card or check by email and also make a payment with our business checking account at Bank Of America We Help You get to Where you want to Take Your FIco Score Visit Our Website Today and Find out what Quality Trade Lines can do for you www.qualitytradelines.com or call 323 776 6424 Testimonial |

QUALITY TRADE LINES

WE PROVIDE TRADE LINES & HELP YOU GET FUNDING WITH CREDIT CARDS AND LINES OF CREDIT Archives

June 2019

Categories |

RSS Feed

RSS Feed